The European Union allows to use a special scheme — "VAT on margin" — when reselling second-hand goods, works of art, collectors' items, and antiques. Under that scheme, the seller has to pay VAT only on the difference between the sales price and the purchase price (the margin). The scheme can be used if the items have been purchased from an original creator or any other non-VAT-taxable person; or, to explain it in other words, if the company has not deducted VAT on that purchase.

Example:

A store accepts a second-hand item for resale and pays the previous owner 60 €. The store will resell the item at 100 €. In this case, the seller's margin is 100 - 60 = 40 €; assuming a VAT rate of 15%, the tax will be 6 € (and the net value is therefore goinfg to be 100 - 6 = 94 €).

For a short overview, with links to the original legislation, please see https://taxation-customs.ec.europa.eu/special-schemes_en.

How to sell second-hand goods in Erply

This feature requires Classic back office.

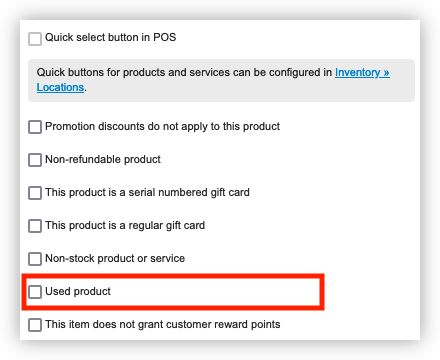

To sell items with VAT on margin, please check the box "Used product" on the product card in Erply back office:

When selling that item, Erply will calculate the taxable value as the difference between the sales price and the FIFO cost of that item, and will calculate VAT based on that.

We strongly recommend to create a separate product card for EACH second-hand item, and label each such item with a unique barcode. Each second-hand item usually anyway has unique properties (not just objects of art, but even refurbished appliances) and might have been purchased for a different price; there is no reason to treat them as equal and let FIFO work out the costs.

To help follow that principle, Erply will automatically archive a second-hand product once it has been sold.

One important thing to keep in mind: Erply does not, unfortunately, have a way to store the item's final sales price with VAT. The product catalog contains just net prices. Therefore, in the above example, to get the expected selling price of 100 €, it is necessary to create the product record (or import it) with a net price of 94 €, thus anticipating that its cost is 60€ and that it is going to be sold under the "VAT on margin" scheme. (This is one more reason to create a separate product card for each second-hand item). The back office product form will initially display an incorrect price with tax, assuming that the whole 94 € will be taxable; the actual sale will work out correctly.